Summary

The March retail sales report met expectations on the headline and exceeded expectations after accounting for upward revisions to prior data and a composition of spending that reflects more than just a pre-tariff splurge. The upshot is that Q1 PCE is shaping up to be halfway decent.

Reality is something that you rise above

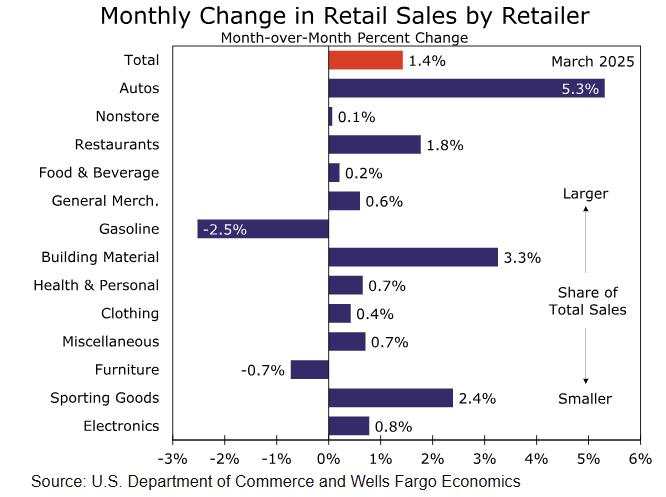

Worries about tariffs may be weighing on confidence and lowering expectations to levels not seen since the financial crisis, but you'd be hard-pressed to find evidence of that in today's retail sales report. Retail sales jumped 1.4% in March and while some gain is attributable to a pull-forward in demand ahead of tariffs, the underlying details suggest consumers are still spending.

Yes, some households are getting major purchases in before tariffs bite. The biggest gainer in today's report is autos (+5.3%) where vehicles are moving off dealer lots faster than at any time since the post-pandemic demand surge earlier this decade. Households are also hitting up their local garden supply & building material stores where receipts grew 3.3% in March.

So yes, consumers are playing a bit of beat-the-clock with tariffs, but there is more to the story here. It may be difficult to reconcile, but once again, consumer spending is managing to avoid the gravitational pull of all the negative dynamics that might otherwise hold it back.

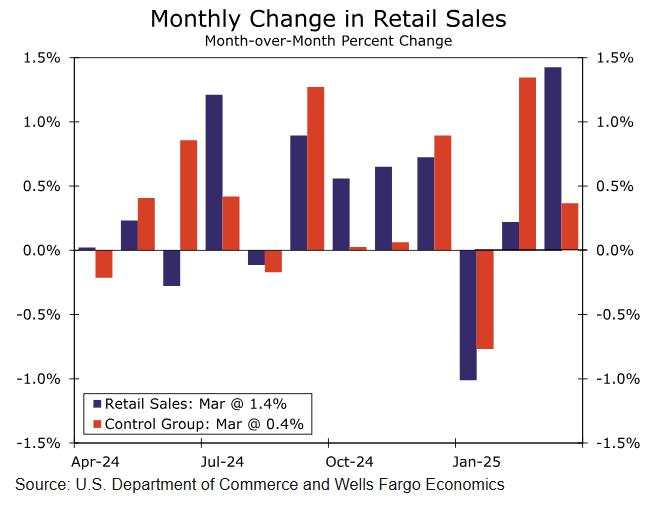

Recall that the worst of the recent equity market volatility did not take place until April. March was simply a strong month for retail sales. The only categories in decline were either small ones (furniture stores and department stores) or price related (gas stations) (chart). The broad-based spend in March comes even as February sales were revised higher. In fact, control group sales were revised up three tenths to reveal a 1.3% pop in February after a sizable drop to start the year (chart).

This measure strips volatile components (sales at auto dealers, building material stores, gas stations and restaurants) that are accounted for elsewhere in GDP and is a good indication of broader goods consumption. After the volatile start to the year, control sales rose a trend-line 0.4% in March, which tells us consumers keep spending. This should provide some support for first quarter spending and suggests even as consumers have front loaded some big purchases, they're still spending on retail.

Consumers also spent more at restaurants in March, and we're not aware of a way you can front-run tariffs with a nice night out. Sales at food services & drinking places leaped 1.8%, a key signal that while spending may be slowing consumers have not gone into hiding when it comes to discretionary spending. We don't read too much into the pullback in gasoline sales, which looks mostly price related.

How consumers act in these next couple of months will be telling. To the extent recent strength is due to a conscious pull-forward in demand, we may be due for some serious payback in April and May. A household that bought a car in March ahead of tariffs, likely isn't buying another one in May. In fact the new car payment might curtail spending in other categories.

It also remains to be seen how consumers act in the wake of tariffs. Even as tariff policy is broad based, the consumer inflation impact may take some time to show up. Consumer optimism has slid amid tariff-related pricing concerns, but one of the lessons of the pandemic was that what consumers say is seldom the best barometer for actual spending.

Download The Full Economic Indicator

作者:Wells Fargo Research Team,文章来源FXStreet,版权归原作者所有,如有侵权请联系本人删除。

风险提示:以上内容仅代表作者或嘉宾的观点,不代表 FOLLOWME 的任何观点及立场,且不代表 FOLLOWME 同意其说法或描述,也不构成任何投资建议。对于访问者根据 FOLLOWME 社区提供的信息所做出的一切行为,除非另有明确的书面承诺文件,否则本社区不承担任何形式的责任。

FOLLOWME 交易社区网址: followme.asia

加载失败()